Two Lenses on the Same Housing Question

Berkshire Hathaway HomeServices’ 2026 outlook is cautiously optimistic for buyers, citing lower mortgage rates, rising inventory, and improved buyer leverage.What their reports don’t include is a real-time, market-implied probability layer on key inputs like Fed rate decisions. Smart Bet Insider combines prediction market data with traditional forecasts to highlight where consensus aligns or diverges.

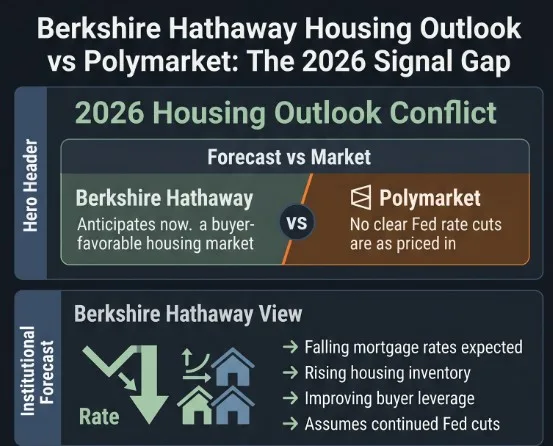

The Berkshire Hathaway housing forecast depends fundamentally on the Fed rate path — and Polymarket’s rate markets are currently pricing a significantly more cautious outlook on rate cuts than the optimistic scenario their 2026 forecast was built on. That divergence is the most important housing market signal in the prediction market ecosystem right now.

What Berkshire Hathaway HomeServices Is Forecasting for 2026

The HomeServices of America 2026 National Housing Outlook identifies four primary drivers of improving buyer conditions: continued mortgage rate declines from anticipated Fed rate cuts, rising home inventory across major metros, stagnant or declining new listing prices, and increasing seller willingness to negotiate.The report cited housing costs falling in 31 of the top 50 largest metros as evidence that buyer leverage was meaningfully improving — a notable structural shift from the seller-dominated market of 2022 and 2023. Three consecutive Fed cuts in September, October, and December 2025 brought the federal funds rate from 4.25–4.50% to 3.50–3.75%, with Goldman Sachs Research anticipating further cuts through 2026.

Mortgage rates had already moved from the 6.9% average of 2024 toward approximately 6.0–6.26% by early 2026. Berkshire Hathaway HomeServices noted that dropping a full percentage point on a mortgage rate can reduce a monthly payment by nearly 20% — making the anticipated continuation of rate cuts central to their buyer-favorable outlook.

What Polymarket Is Currently Pricing on Fed Rate Cuts

The prediction market consensus on Fed rate policy in 2026 has shifted meaningfully away from the optimistic rate-cut scenario that underpins Berkshire Hathaway’s housing forecast. Polymarket’s “How many Fed rate cuts in 2026?” market is currently pricing elevated probability on zero additional rate cuts, reflecting the FOMC’s April 2026 decision to hold the federal funds rate steady at 3.50–3.75% with core PCE inflation running near 3.2%.

The June 2026 FOMC decision market has the “No change” contract trading at approximately 98%, reflecting near-unanimous market consensus that the Fed will hold rates steady at its June 16-17 meeting. Polymarket’s “Fed rate hike in 2026?” market assigns 32% probability to a rate increase before year-end — a scenario that would directly reverse the mortgage rate trajectory Berkshire Hathaway’s forecast depends on.

The combination of sticky inflation, stable unemployment near 4.3%, and growing political pressure on the Fed has produced a rate market environment that is materially less accommodative than the 2026 scenario Berkshire Hathaway’s housing outlook assumed.

The Mortgage Spread Regime: Why Fed Cuts Don’t Directly Translate to Housing Relief

Most housing commentary still relies on a simplified transmission story: Fed rate cuts lead to lower mortgage rates, which then unlock housing demand. In practice, that relationship has weakened significantly. Mortgage pricing in 2026 is better understood through a mortgage spread regime, where the federal funds rate is only an indirect input rather than the primary driver.

The 10-Year Treasury as the Real Anchor

The 30-year mortgage rate is anchored far more tightly to the 10-year Treasury yield than to Fed policy itself. Treasury yields reflect inflation expectations, growth risk, and term premium dynamics — all of which can diverge from Fed decisions for extended periods. The FRED 10-year Treasury series shows frequent episodes where yields rise or fall independently of policy stability, making Fed rate contracts an incomplete signal for mortgage rate forecasting.

The MBS Spread Layer

On top of the Treasury baseline sits the mortgage-backed securities (MBS) spread, driven by liquidity conditions, prepayment risk, and Federal Reserve balance sheet demand. The New York Fed’s agency MBS operations highlight how directly central bank participation affects mortgage pricing beyond policy rates alone. These spreads can widen even when the Fed holds rates steady — pushing mortgage rates higher despite a “no change” policy outcome.

The Dual-Layer Pricing System

This is why the 30-year mortgage rate series often decouples from Fed expectations entirely. The result is a dual-layer pricing system: Treasury yields set the macro direction, while MBS spreads determine the financing premium on top. The key implication for interpreting Berkshire Hathaway’s housing outlook is direct — the forecast implicitly assumes clean pass-through from Fed easing to mortgage relief, but the real variable is the mortgage–Treasury spread regime, which prediction markets like Polymarket do not directly price. Fed contracts capture policy probability, not the liquidity and risk premia that ultimately determine housing affordability.

What the Prediction Market Divergence Means for Buyers and Sellers

The gap between Berkshire Hathaway HomeServices’ buyer-favorable 2026 forecast and Polymarket’s current rate pricing creates a practical interpretive challenge for anyone making housing decisions in 2026. The Berkshire Hathaway outlook was built on a rate-cut trajectory that prediction markets are no longer pricing as the base case.

Zero additional cuts in the current Polymarket consensus suggests mortgage rates may stay near 6%, limiting affordability gains despite rising inventory. While Berkshire Hathaway’s supply-side outlook still holds, the key divergence is on affordability: expected rate relief that would expand demand may not materialize in 2026 if the Fed holds longer than markets anticipate.

Smart Bet Insider: Using Prediction Market Data to Interpret Institutional Forecasts

The Berkshire Hathaway HomeServices housing outlook and Polymarket’s Fed rate markets are complementary analytical layers that address different parts of the same question. Berkshire Hathaway provides structural housing market analysis built on qualitative and quantitative real estate data. Polymarket provides real-time, capital-backed probability estimates on the macroeconomic inputs that feed the structural analysis.

Smart Bet Insider’s macroeconomic prediction market coverage tracks the Polymarket Fed rate markets, inflation contracts, Treasury yield markets, and their implications for asset classes including real estate — delivering the integrated macro picture that neither institutional real estate forecasts nor prediction market data provides alone.

Follow Smart Bet Insider today and approach every macroeconomic prediction market with the analytical framework that connects financial market signals to real-world asset implications.

Conclusion: The Forecast and the Market Are Telling Different Stories

Berkshire Hathaway HomeServices’ 2026 housing outlook and Polymarket’s Fed rate pricing are both legitimate, data-grounded signals — and they are currently pointing in different directions on the most important variable in the housing equation. The structural buyer improvements Berkshire Hathaway identified are real. The rate-cut acceleration that was supposed to amplify those improvements is not the base case on Polymarket’s current pricing.

Understanding where institutional forecasts and prediction market pricing diverge is precisely the kind of analytical edge that separates reactive market participants from prepared ones. Smart Bet Insider delivers that integrated macro perspective — connecting prediction market probability signals to real-world asset implications across housing, equities, and fixed income. Follow Smart Bet Insider now and interpret every institutional housing forecast with the real-time prediction market context it demands.

FAQs

What is Berkshire Hathaway HomeServices’ 2026 housing market forecast?

The HomeServices of America 2026 National Housing Outlook projects improving buyer conditions driven by rising inventory, stagnant new listing prices, increased seller negotiating flexibility, and declining mortgage rates. The report cited housing costs falling in 31 of the top 50 largest metros and identified late 2025 as a potential turning point favoring buyers — a forecast built substantially on the assumption of continued Fed rate cuts through 2026.

What does Polymarket say about Fed rate cuts in 2026?

Polymarket’s rate cut market is currently pricing elevated probability on zero additional rate cuts in 2026, reflecting the FOMC’s April hold at 3.50–3.75% with core inflation near 3.2%. The June FOMC decision market has “No change” at approximately 98%, and the “Fed rate hike in 2026?” market assigns 32% probability to a rate increase before year-end.

How does the Polymarket Fed outlook affect the Berkshire Hathaway housing forecast?

Berkshire Hathaway’s buyer-favorable 2026 forecast was built on an assumption of continued rate cuts driving mortgage rates lower. Polymarket’s current pricing implies a prolonged hold — meaning the mortgage rate relief that was expected to expand the buyer pool may not materialize as projected. Structural improvements in inventory and pricing still hold, but the affordability catalyst depends on a rate path the market is no longer pricing as base case.

What is the Mortgage Rate Transmission Gap?

The Mortgage Rate Transmission Gap is the delay and imperfect correlation between changes in the federal funds rate and changes in 30-year fixed mortgage rates. Mortgage rates track 10-year Treasury yields rather than the Fed funds rate directly, meaning the Fed rate path is a necessary but not sufficient input for predicting mortgage rate movements. Use both the Fed rate and Treasury yield markets to build complete mortgage rate forecasts.

Where can I track Polymarket’s Fed rate markets?

The full suite of Fed rate prediction markets is available at Polymarket’s Fed Rates page, covering June decision markets, full-year cut count markets, and rate hike probability contracts. Combined trading volume across these markets exceeds $48 million, reflecting genuine institutional and retail engagement with real capital backing the implied probabilities.

Does a Fed hold in 2026 mean the housing market gets worse?

Not necessarily — a Fed hold at 3.50–3.75% preserves the rate improvements already achieved through the 2025 cut cycle. Mortgage rates near 6% are significantly lower than the 7%+ environment of 2023, and the structural inventory improvements Berkshire Hathaway identified remain intact regardless of the rate path. The downside is that further rate cuts pushing mortgage rates toward 5.5% may not arrive in 2026.

Can prediction markets forecast housing prices?

Prediction markets don’t currently offer direct housing price contracts, but they price the most important inputs to housing market forecasts: Fed policy, inflation, recession probability, and economic data releases. Tracking these markets and mapping them to housing market drivers provides a more current and capital-backed probability layer than traditional institutional forecasts, which are typically published quarterly rather than updated in real time.